Image generated using Microsoft copilot

Northern Ireland has entered 2026–27 without an agreed Budget. That is unusual, and almost certainly undesirable, but not unprecedented.

As set out in our latest Sustainability Report (16 June 2026), departments can continue to spend for the time being. But operating without a Budget alters how the system functions, weakens normal budget management and democratic accountability, and introduces additional risks.

In the absence of a Budget, the Department of Finance has issued planning envelopes to each department to guide their spending. But they are not firm limits and individual Ministers may believe they are insufficient and behave as such.

Keeping public services running

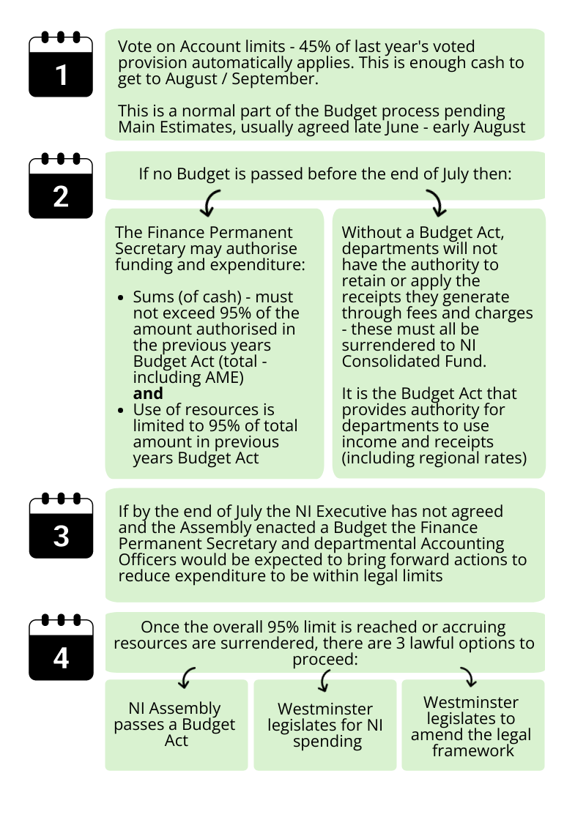

Even without an agreed Executive Budget or Budget Act, departments can spend.

At the beginning of the fiscal year, spending is governed by the Vote on Account, which provides interim legislative authority for departments to draw cash and use resources—typically up to around 45 per cent of the amounts authorised in the previous year’s Budget Act.

If a Budget Act has not been passed by the end of July, statutory contingency provisions are engaged. Under section 59 of the Northern Ireland Act 1998 (cash) and section 7 of the Government Resources and Accounts (Northern Ireland) Act 2001 (resources), the Department of Finance Permanent Secretary may authorise continued spending beyond the 45 per cent level.

These powers allow departments to continue operating for the remainder of the year, but only within strict aggregate limits. The total cash issued cannot exceed 95 per cent of the amount authorised in the previous year’s Budget Act — £27.4 billion in 2025–26 — and the same 95 per cent limit applies to the use of resources, which totalled £30.9 billion.

In practice, this means departments must work within a reduced version of last year’s voted provision: the full set of Assembly-approved limits for resource and capital Departmental Expenditure Limits (DELs, which cover spending on public services, administration and investment), Annually Managed Expenditure (AME, which largely covers demand-led spending on social security benefits and pensions) and associated cash.

AME sits outside the departmental planning envelopes, but inside the legal contingency limit. So, if demand-led spending on benefits or pensions rises, beyond the Executive’s control, it uses up some of the overall 95 per cent headroom and increases the pressure on DEL-funded services.

These mechanisms are designed to avoid a “hard stop” in public services. They are not a substitute for a Budget. Rather, they ensure services can continue to operate while agreement on a Budget is secured.

Figure 1 – the budget process and contingency powers

Why a Budget still matters

Operating without a Budget weakens two key features of normal public finance management:

1. Democratic accountability is reduced

A Budget Act sets out allocations agreed by Ministers, and scrutinised and authorised by the Assembly. In its absence, spending continues - but without the same level of transparency or political legitimacy.

2. Financial risks increase

The contingency framework introduces hard constraints and potential shocks:

- Spending is capped at 95 per cent of last year’s enacted totals.

- Departments must manage rising costs—particularly pay—within that limit.

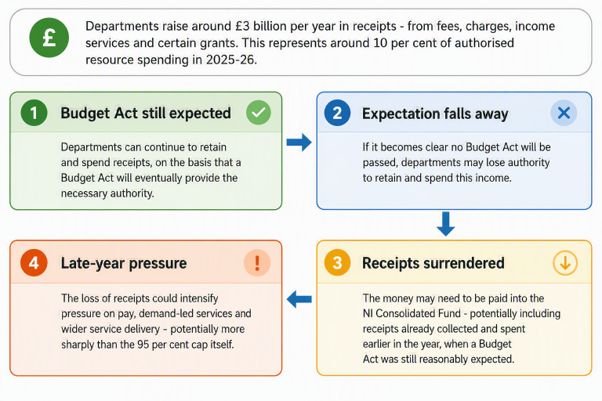

- And, critically, they may lose access to income they generate themselves.

This last point may be the most significant. Departments raise around £3 billion per year in receipts (e.g. fees and charges, income from services and certain grants). Without a Budget Act, they may lose the authority to retain and spend this income. For context, this represents approximately 10 per cent of the Executive’s total authorised resource spending for 2025-26.

So long as there continues to be a reasonable expectation that a Budget is agreed before the end of the financial year, departments can continue to spend these receipts. However, if it becomes clear that will not happen, these funds must be surrendered back to the central pot (the NI Consolidated Fund). This includes receipts already collected and spent earlier in the year, when departments were still reasonably expecting a Budget Act to be passed.

At that point, pressures on departments would intensify sharply—potentially in a more binding way than the 95 per cent cap itself. The loss of receipts would affect the ability to meet pay commitments, fund demand-led services and maintain service delivery late in the year.

Figure 2 – the £3 billion receipts risk

Planning in uncertainty: the role of envelopes

In the absence of a Budget, the Department of Finance has issued contingency planning envelopes to departments.

These are not spending limits. They are planning tools—intended to provide a “reasonable working assumption” of what departments might receive in a future Budget.

Key features:

- They cover resource and capital DEL only (not demand-led spending such as benefits or pensions).

- They are not formal expenditure limits and do not, by themselves, prevent departments from spending more. This creates a governance risk: spending may continue above the planning assumptions in the early part of the year, especially where Ministers are reluctant to reduce services or defer pay-related pressures. But spending more now would leave less room to manoeuvre once formal limits are imposed, increasing the risk of sharper late-year action, Ministerial Directions or overspending against wider controls.

- A separate capital position has also been set out, with capital allocations largely based on previously agreed projects with limited flexibility remaining.

Around £620 million of resource DEL and £819 million of capital DEL remain unallocated at this stage, but this should not be read as freely available headroom. For resource DEL, some funding is expected to be held centrally for specific commitments, including repaying the Treasury Reserve claim, transformation, debt interest and other Executive programmes. The purpose of leaving funding unallocated is therefore less about creating spare capacity, and more about preserving the Executive’s ability to adapt allocations if a Budget is eventually agreed, without immediately having to cut departmental planning envelopes already issued.

In effect, the system is trying to recreate some of the discipline of a Budget—without actually having one.

Who is in control?

The absence of an agreed Budget creates an unusual tension between legal authority, financial control and political accountability.

Accounting Officers are expected to act prudently: to plan within the funding that can reasonably be expected, manage spending within lawful limits, and bring forward options to reduce or delay expenditure where necessary. In the current circumstances, that may mean advising Ministers that some spending cannot safely continue at the level they would prefer.

Ministers, however, remain politically accountable for public services. They may judge that pressures — particularly on pay, statutory services or frontline delivery — require spending to continue, even where officials believe this creates a risk of breaching the limits set by the Finance Permanent Secretary.

Where that disagreement cannot be resolved, Ministers can issue Ministerial Directions, instructing officials to proceed despite concerns about regularity, affordability or value for money. Directions do not make the underlying pressure disappear; rather, they make explicit that Ministers have chosen to accept the risk.

This is not a hypothetical concern. Directions were used in 2025–26 to fund pay awards in Health and Education, contributing to overspending that was later only met through a claim on the Treasury Reserve. In the absence of an agreed Budget for 2026–27, similar tensions could become more acute: Accounting Officers may seek to contain spending within constrained contingency limits, while Ministers may resist reductions that would affect pay or services.

Short-term cover, longer-term uncertainty

This uncertainty extends beyond the current year. The Budget that was not agreed was intended to cover three years, and the savings and funding gaps identified by departments also run across that period. But the contingency mechanisms are single-year bridges: they can keep spending lawful for 2026–27, but they cannot provide the certainty needed for multi-year transformation, capital planning, workforce decisions or pay reform. In practice, that makes it harder to deliver savings sustainably and increases the risk that difficult choices are deferred rather than resolved.

The scale of the challenge

Even with planning envelopes and proposed savings, the gap remains large.

Departments have identified significant efficiency and savings measures, but there is still a shortfall of around £1.4–£1.6 billion per year between available funding and the amounts that departments say they need.

Closing that gap will require:

- reducing services,

- increasing revenues, or

- securing additional funding.

Operating without a Budget does not remove these choices. It simply delays them—and makes them harder.

The bottom line

The absence of a Budget is both a fiscal and a political problem.

Contingency powers and planning envelopes can keep the system operating for a time. But they cannot resolve underlying pressures.

At some point, decisions will be required—on spending, on revenue, or both. In that sense, the real challenge is not simply agreeing a Budget. It is agreeing one that can be sustained.