If we want a clear account of NI’s public finances, the NI National Insurance Fund must sit in plain sight. It is not an accounting footnote. It is a major source of cash for welfare benefits and the health service, operating alongside Supply – the funding voted annually by Parliament, authorising NI departments to draw money from the Consolidated Fund. Pull it into the frame, and the numbers make far more sense.

Ask people how NI’s public services are paid for, and most will say “the Block Grant and the Rates.” But that is not the full story. Sitting alongside the Executive’s voted Budget is a separate pot of money that moves billions each year without much fanfare: the NI National Insurance Fund (NIF). It is where National Insurance contributions paid by NI citizens land, and from where the State Pension and other contributory benefits are paid. It also sends cash directly into NI departments, outside the usual Supply process.

We began looking closely at the NI National Insurance Fund while reconciling different accounts of NI’s public finances. In particular, we found a persistent gap between estimates of UK Government funding and the cash actually recorded in the NI Consolidated Fund. Understanding the role of the NIF turned out to be essential to resolving that gap.

What the Fund is—and how it flows

Every payday, employees and employers in NI pay National Insurance. HMRC first carves out an allocation for the Department of Health (DoH) to support the NHS in Northern Ireland, then pays the remainder into the NI NIF. This NHS share is set after consultation with the Government Actuary’s Department and approval by HM Treasury, reflecting long standing legislation governing the scheme.

The Fund then finances contributory benefits and the State Pension, administered in NI by the Department for Communities (DfC), which also has its administration costs reimbursed by the NIF. So the NIF is not just a ledger entry: it is a cash pipeline funding real entitlements and part of the health service’s day to day costs.

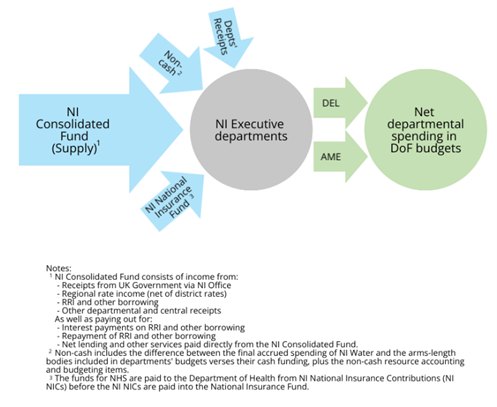

Figure 1 - Flows of money in and out of the NI Executive

The numbers—at a glance

The scale is bigger than most people realise - the flow of cash through the NIF is larger than the annual spend by the Department of Education, NI’s second largest spending department after Health. As illustrated in Figure 1 above, the NI NIF financed about £4.3 billion of NI departmental spending in 2023-24, which is 13 per cent of the funding flowing into NI departments. The main areas it financed are broken down in Table 1 below. Around 80 per cent is allocated as Resource Annually Managed Expenditure (AME) benefit spending, which is paid directly to individuals and households. The bulk of the rest is resource Departmental Expenditure Limits (DEL) NHS spending paid directly to the Department of Health. None of this requires a vote of Supply from the NI Consolidated Fund - it arrives as non voted funding direct from the NIF.

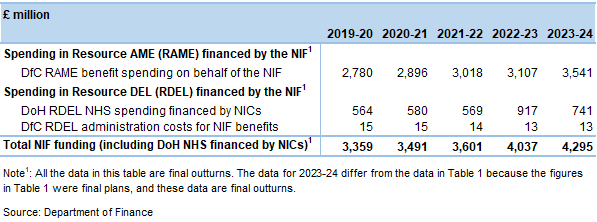

Table 1 - Spending in DfC and DoH budgets financed from the NIF

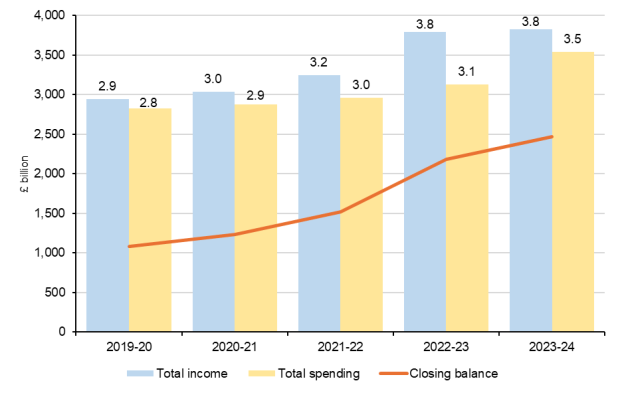

On the Fund’s own account, income has grown from just under £3.0 billion in 2019–20 to about £3.8 billion in 2023–24, while the closing balance rose from roughly £1.1 billion to nearly £2.5 billion over the same period. That balance is actively managed to keep NI’s share at 2.77 per cent of the combined GB and NI Funds, rather than reflecting the contributions specifically raised in NI in any given year. Delivering this requires regular transfers from the GB NIF, given higher per capita NICs in GB. Over the last five years, those transfers made up about 20 per cent of NI NIF income.

Chart 1 - NI NIF income, spending and closing balance

Why this changes how we read the Budget

At first glance, the Executive’s Budget suggests that day to day spending (DEL) is funded by the Block Grant plus the Rates. But “Block Grant” is a spending limit - a control total - not a cashflow. In cash terms, departmental spending is financed from two sources: voted Supply from the NI Consolidated Fund, and non-voted flows from the NIF — notably DoH’s NHS resource spending funded from NICs and DfC’s costs of administering NIF benefits. Seeing that overlap stops us double counting and explains why some spending never appears as a draw on Supply.

This matters for transparency. When completing chapter 5 of our comprehensive guide to NI’s public finances we initially found a persistent gap between estimated UK Government funding (from Treasury’s PESA) and the actual receipts recorded in the NI Consolidated Fund. The missing piece turned out to be the NI NIF. In 2019–20 the gap was about £3.5 billion (and £4.3 billion by 2023–24); once NIF flows were added, the picture largely reconciled. Small differences remain due to timing and non cash measurement, but they are now understood and modest.

The fuller picture of “money in”

The NI NIF underwrites entitlements that must be paid, and channels earmarked health funding via NICs, which means that parts of DEL spending are in effect financed off Budget (in cash flow terms) even though they sit inside the Block Grant control total.

For the public, it is about understanding where your contributions go. Your NICs support today’s pensions and contributory benefits in NI and help fund the NHS. That mix of contributions, interest earnings and transfers from GB keeps the Fund on a sound footing so that payments are made when due.

Recognising the NI NIF also helps place other overlooked income in context. Departmental receipts - fees and charges, loan repayments, EU funds and more - were just under £2 billion in 2023–24, more than twice gross Regional Rates income (around £0.8 billion). Some of those fees are internal payments within the public sector, but the point stands: the Executive’s finances are broader than the traditional Block Grant plus Rates story, and the NIF is a central reason why.

Further information

You can find a fuller treatment of this topic in our NI National Insurance Fund Technical Paper.

As with all our publications, we welcome any questions, thoughts or feedback. Please get in touch with us through info@nifiscalcouncil.org

Glossary

In this quick read, we refer to several technical public expenditure concepts. A short explanation of each is set out below. Our comprehensive guide to NI’s public finances and the Department of Finance’s Public Expenditure Terminology guide also helpfully unpack these terms.

The Northern Ireland Consolidated Fund (NICF)

This is the main cash account for NI central government. It is the route through which cash is received and issued for devolved public spending, and it underpins the legal authority (“Supply”) to spend that cash once voted by the Assembly.

Supply

The legal authority and the cash that government bodies draw from the Consolidated Fund to finance their spending in‑year. The Assembly gives this authority through Supply (Appropriation) Acts after it considers the Main Estimates and any Supplementary Estimates. In short, supply = cash that has been authorised for departments to spend.

NI context: The Northern Ireland Office pays a cash grant into the NI Consolidated Fund, and—once the Assembly votes the Estimates—the Department of Finance issues Supply to departments to meet their net cash requirement.

Voted (expenditure / provision)

Spending that appears in the Estimates and is explicitly authorised (“voted”) by the Assembly via the Budget/Supply Acts. It sets the limits and purposes (“ambits”) for how much each department can spend and on what.

NI context: The bulk of departmental DEL and AME sits in the Estimates and is therefore voted. Once voted, it is financed in cash by Supply from the NI Consolidated Fund.

Non‑voted (expenditure / funding)

Spending not included in the Estimates because it is financed directly from another source or is authorised under separate standing legislation, so it does not require an Assembly vote in the Estimates. It therefore does not draw on voted Supply.

NI context: As set out above, NI National Insurance Fund (NIF) financing for DfC’s contributory benefits (Resource AME) and DoH’s day‑to‑day NHS spending (Resource DEL) are non‑voted (no Supply).