Behind every turn of the tap in Northern Ireland lies a water system straining between rising expectations and tightening budgets.

NI is unusual in the UK for not charging households for the water they use. In England and Wales households pay the water companies directly, while in Scotland water charges are collected alongside council tax. Since NI Water was established in 2007 as a publicly owned monopoly, the Department for Infrastructure (DfI) and its predecessor departments have paid the company a subsidy in lieu of domestic water charges. This is despite the commonly held view that households already contribute through the domestic rates bill. This reduces the amount that the Executive can spend on other public services. That choice—popular then and still politically sensitive now—helps determine how quickly new homes can be approved, how much pollution is tolerated and where in NI businesses choose to locate.

Our report on the fiscal sustainability of the NI water industry argues that without new, reliable funding, investment will lag behind what is needed—especially for dealing with wastewater—constraining economic growth and risking service quality.

What NI Water is (and why that matters)

NI Water is a Government‑owned Company (a “GoCo”) and, crucially, it is classified for budgeting purposes as a Non‑Departmental Public Body (NDPB). That means its day‑to‑day spend (resource) and its investment (capital) both count against DfI’s budget limits. NI Water can “borrow” from the department for capital projects, but that borrowing doesn’t increase the Executive’s budget—it merely changes where funding flows. Even if NI Water has the cash, it cannot exceed the authority to spend (‘budget cover’) that DfI gives it in any year.

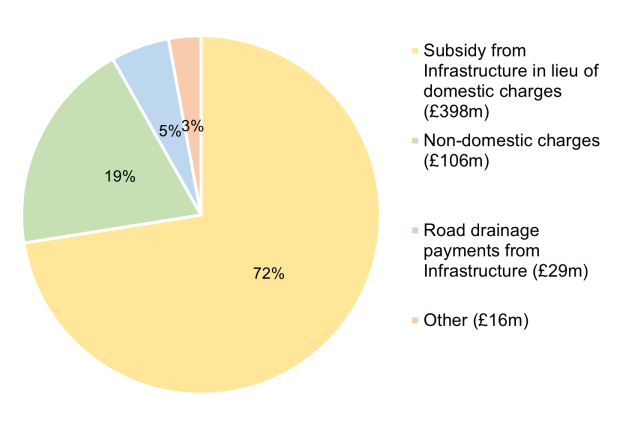

Where the money comes from today

In 2023‑24, NI Water recorded £550 million in revenue. Roughly 70 per cent came from the DfI subsidy in lieu of household bills, roughly 20 per cent from non‑domestic charges paid by businesses, and the rest from roads drainage payments and other income,

NI Water’s income mix (2023–24)

How the system is steered

In the absence of effective competition to protect customers, NI Water is regulated via multi‑year Price Controls (PCs) set by the Utility Regulator (UR). These PCs specify outputs (e.g., water quality, environmental standards), efficiency targets, and what spending would be appropriate to deliver them. The current PC21 runs from 2021‑22 to 2027‑28. The UR judges what NI Water should spend, but DfI decides what NI Water can spend within the Executive’s usually single year budget horizons. In recent years funding has fallen short of the PC recommendation—typically around a quarter below—and that is part of the problem. Even when the need to invest in infrastructure and services is clear and supported by the UR, actual funding depends on the state of the Executive’s budget.

The crunch point in PC21

Midway through PC21, the UR concluded that NI Water would need £1.465 billion of capital spending cover between 2024‑25 and 2026‑27. But DfI advised NI Water to plan for a “reasonable worst‑case” capital scenario of £992 million—a gap of almost a third. In practice, in-year reallocations across Executive departments have ensured a more favourable position than this planning scenario, but funding generally still falls short of what the UR deems necessary. Pressures were also felt on resource budgets (not least from energy prices), though some relief came when wholesale prices eased. The result was to constrain NI Water’s delivery: schemes slowed and wastewater upgrades were deprioritised or pushed into later years.

Why wastewater constraints hit everyone

Stakeholders—from councils to developers—have told the Council that inadequate wastewater capacity has become a handbrake on residential and commercial development and represents a major constraint on economic growth in NI. Wastewater capacity is not just an infrastructure issue: when treatment works or sewer networks reach their limits, new housing and commercial development can be delayed or prevented altogether.

NI Water has identified:

25 hub towns with severely compromised sewerage infrastructure

91 further large towns where wastewater networks are already a serious restriction on new development

Even with full PC21 funding, NI Water estimates it would take around 18 more years of above‑average investment to remove development constraints entirely.

When wastewater works can’t accommodate growth, planning permissions stall and the economy underperforms.

Performance: better—but the bar is rising

NI Water has narrowed historic efficiency gaps with its English and Welsh peers and meets most of its UR‑set output targets. But on pollution (major incidents) it still lags the top rated, and the absolute bar is rising across the UK. In December 2024, Ofwat approved large real bill increases for English and Welsh companies to fund a step‑change in investment—especially to curb storm overflows and tighten wastewater standards. If that delivers, NI Water’s relative performance risks slipping unless it also invests more—yet its funding is constrained by the Executive’s budget, not bills.

What would household charging change?

Introducing domestic water charges would, in effect, flip the model: households would pay NI Water directly for services, and the subsidy currently paid by DfI could be reallocated within the Executive’s budget. UR’s latest estimate of the notional average household bill in 2025‑26 in NI was about £592 (if charging existed). Even after administration and support for low‑income households, DfI estimated that charging would have freed up of the order of £300 million of resource and capital in 2022‑23—and likely more in later PC21 years—though the exact amounts vary with inflation and policy design. However, charging remains politically unpopular and set‑up costs (e.g., metering) could be significant.

For now, Ministers continue to rule out charging.

Changing NI Water’s corporate form requires domestic charges

Two ideas have been floated to change the status of NI Water, but both require greater revenue raising i.e. domestic charges:

- Turning NI water into a Public Corporation (like Scottish Water).

If NI Water raised 50 per cent or more of its costs from commercial revenue, it could be reclassified as a Public Corporation. That would change how its investment shows up in DfI’s budgets (its finance rather than its spend would score), giving some flexibility—plus the ability to hold reserves. But this reclassification is not possible without domestic charging, because NI Water currently only generates around 30 per cent of its income commercially.

- Mutualisation or privatisation.

If NI Water raised 50 per cent or more of its costs commercially and ceased to be controlled by government, it could become a mutual or private company – removing the constraint of departmental budget cover. External borrowing off the public sector balance sheet would, in theory, allow more investment. In practice, public and political appetite for privatisation is low given controversy around performance, debt and dividends among English water firms. Wales’ mutual model (Glas Cymru/Welsh Water) avoids dividends but its performance does not appear significantly stronger.

Recent DfI Ministers have opposed both routes, because domestic charging would be necessary in either case.

The bottom line

The report emphasises that each potential solution involves trade-offs. Continuing with the current subsidy model means that water investment has to compete directly with other public spending priorities in the Executive’s budget. Introducing domestic charges could provide a more stable revenue stream but remains politically contentious. Changing NI Water’s classification or structure could ease some capital-budget pressures, but this would still require a reliable source of revenue. In practice, resolving the funding gap involves balancing affordability, political acceptability and fiscal constraints.

Even so, two things need to change for NI’s water system to deliver high quality wastewater services in the long term.

First, more revenue—whether via domestic water charges or another instrument. Without this, the Executive will keep rationing capital to NI Water while wastewater constrains growth and the bar for service quality rises across the rest of the UK.

Second, predictability: multi‑year, ring‑fenced budget cover aligned to the regulatory cycle would improve value for money and reduce “use‑it‑or‑lose‑it” pressures at year‑end, leading to a more resilient long-term service.

Find out more and get in touch

If you’re interested in the full detail please see our published sustainability report on water. We warmly welcome engagement, feedback and constructive challenge on this analysis and on our wider programme of work. You can contact the team at info@nifiscalcouncil.org